Inflation

Like I wrote in my post “Time value of money“, inflation is destroying the value of your money. In this learning-post I will show you simple examples how to calculate the effects of inflation. Inflation rate is based on yearly difference in Consumer Price Index (CPI).

Example. 1

You have $10 000 in your bank account and you want to keep it there as an emergency fund. After three years you are calculating its purchasing price. You find out that inflation rate was 3% in all these years (it’s rarely exactly the same). So, how much is that $10 000 worth compared to the baseline?

Formula for calculating this is A / (1+r)^t, where A is the amount of money, r is the inflation rate and t is the time in years.

$10 000 / (1+0,03)^3 = $9 151.42. The purchasing power has lowered about $848.58.

If you could buy something three years ago with a price of $ 9151.42, you would now need $10 000 to buy it. Of course inflation rate is an average number, so that isn’t the case with individual products

Common mistakes that I want to point out:

First, some people use formula A * 0,97 when calculating 3% inflation, but this is wrong. Instead you should use A / (1,03) like shown above. That is because inflation means how much more money you need later to be able to buy the same amount of something as before.

So when inflation is 3%, you need 3% more money after a year to remain equal purchasing power ($10 000 * 1,03 = $10 300). And when you calculate that another way around, you get the amount that had equal purchasing power a year ago as your amount right now

($10 300 / 1,03 = $10 000). And this is what you need to calculate.

Second mistake is summing up percent numbers of different years. If there is three years in a row with 3% inflation, like in the example, it is not 9% total inflation in this time period. Instead it’s 1,03 * 1,03 * 1,03 = 1,0927) 9,27%, because after a year the prices have already gone up 3%, so it’s then 103% of the original price. Next increase of 3% doesn’t only take account the original 100%, but also the additional 3%, so it goes up to 106,09% of the original price, and so on.

Example 2.

You have the same $10 000 in your bank account for three years. The inflation rate was 4% in the first year, 5% in the second and 2% in the third year. So, how much is that $10 000 now worth compared to the baseline?

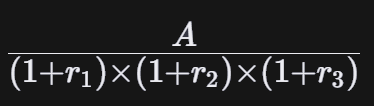

Now when the inflation rate isn’t the same for all those years, you need to calculate those years separately. You can do this with this formula

Where A is again the amount of money and different r-letters represent the inflation rates for each year. You start by multiplying the ratios below 1.04 * 1.05 * 1.02 = 1.11384. Then divide the amount of money with this rate $10 000 / 1.11384 = $8 977.95. The purchasing power has lowered $1 022.05.

Discounting

Discounting works very similarly to inflation but it’s used to calculate different thing. In “Time value of money” there was an explanation of risk-free rates. These are very important in discounting. Well, discounting is used to discount future cash flows into this moment.

Example 1.

If you know you are going to get $1 000 after a year, you would discount it to get its present value (PV). If the risk-free rate for 1-year is 5%, then you would discount that $1 000 with 5% discount rate.

This is done with a following formula:

PV = FV / (1+r)

Where PV is the present value, FV is future value (in this case $1 000) and r is used discount rate (5%).

PV = $1 000 / (1+0.05) = $952.38

So your future cash flow of $1 000 has a present value of $952.38. This basically means you should invest that amount ($952.38) with 5% risk-free rate in order to have $1 000 after a year.

If you had a choice of getting that $1 000 after a year or getting a little bit less right away, you should take any amount bigger than $952.38 right away and invest it in risk-free bonds to have more than $1 000 after a year. If the amount is less than that, you should take the $1 000 later.

To understand this better, you can turn the formula around and calculate the Future value.

FV = PV * (1+0.05) = $952.38 * 1.05 = $1 000

Example 2.

Let’s say you are going to have $1 000 after three years and risk-free rate for this time would be 6%. Now its present value would be

PV = FV / (1+r)^t, where t is time in years

PV = $1 000 / (1+0.06)^3 = $839.62

As you can see, the further in the future the cash flow is, the smaller its present value. This is due to multiple year discounting and nature of risk-free rates that usually go higher as their duration increases.

Discount rate isn’t always based on risk-free rates, but for an individual investor it’s a really good measurement. When companies are considering their investment decisions, they usually use discount rate based on their Weighted Average Cost of Capital (WACC). I’ll explain that more precisely in my future posts

Net Present Value (NPV)

When individual investor or a company is comparing their investment options they usually use Net Present Value calculations. Very important part of these calculations is discounting that you just learned more about. To put it shortly, if NPV is positive, the investment is profitable. This means that all discounted future cash flows added together would be a larger sum than the original investment.

Example 1.

Let’s say you have two options to invest $10 000:

1. Three year bond with a risk-free rate of 7% and yearly payments

2. A loan for a start-up that promises you a 20% return after 3 years (start-ups are risky, so you would expect higher return)

First let’s calculate NPV of the first option:

Year 0 cash flow = -$10 000 (original investment = acquisition cost)

Year 1 cash flow = $10 000 * 0.07 = $700 (7% payment for the bond)

Year 2 cash flow = $10 000 * 0,07 = $700

Year 3 cash flow = $10 000 * 0,07 + $10 000 = $10 700 (in the last year you also get back your original investment when talking about bonds)

Every years cash flow needs to be discounted:

Year 0 = -$ 10 000 (no discounting, since it’s the current moment)

Year 1 = $700 / (1+0.07) = $654.21

Year 2 = $700 / (1+0.07)^2 = $611.41

Year 3 = $10 700 / (1+0.07)^3 = $8 734.38

Then the NPV calculation itself:

NPV = -$10 000 + $654.21 + $611.41 + $8 734.38 = 0$

The value of 0$ means that it’s right there in the limits. That’s because we used the risk-free rate as a discount rate, which is also our rate of return. That means that if we use risk-free rate as a discount rate, we are comparing if the investment is more profitable than investing in risk-free bonds.

Now let’s calculate the second option:

Year 0 cash flow = -$10 000 (original investment = acquisition cost)

Year 1 cash flow = $0

Year 2 cash flow = $10

Year 3 cash flow = $10 000 * 0,20 + $10 000 = $12 000 (Again you get back your loan as well as your 20% return)

Every years cash flow needs to be discounted:

Year 0 = -$ 10 000

Year 1 = $0

Year 2 = $0

Year 3 = $12 000 / (1+0.07)^3 = $9 795.57

Then the NPV calculation:

NPV = -$10 000 + $0 + $0 + $9 795.57 = -$204.43

In this case the investment isn’t profitable. If you get better results with a risk-free investment, there isn’t any rational reason to invest in something with a considerable risk.

These are only incredibly simple examples, but I think they are excellent for understanding why and how they are used in an investment decision situations.

NPV calculations can also be made with WACC or ROE (return on equity) as a discount rate. This will give companies and investors a chance to compare new investments to their financial risks and historical returns.

Be sure to check out my Investors Dictionary to better learn these complex abbreviations and their meanings! Thank you for reading and I hope you tell me your opinion about these examples in the comments below, so I can keep improving and offer you better content in the future!

Leave a comment